Operating profit for the quarter was US$507 million compared to US$552 million in the preceding quarter. The decrease is driven by gain on sale of the West Janus in the first quarter, offset by lower operating and SG&A expenses during the second quarter.

* Seadrill reports its best operating results and net income ever and generated second quarter 2013 EBITDA*) of US$665 million

* Seadrill reports second quarter 2013 net income of US$1,750 million and earnings per share of US$3.68

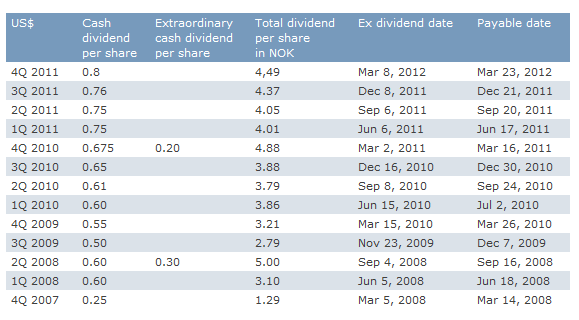

* Seadrill increases the ordinary quarterly cash dividend by 3 cents to US$0.91

* Economic utilization for floaters increased to 94% in Q2 2013 from 92% in Q1 2013

* Economic utilization for the jack-up fleet in Q2 2013 was 98%, down from 99% in Q1 2013

* Seadrill secured a three-year contract for the newbuild drillship West Neptune with a total estimated revenue potential of US$662 million

* Seadrill realized a gain of US$1,256 million from the sale of the tender rig division to SapuraKencana Petroleum for a total consideration of US$2.9 billion

* Seadrill completed the sale of the tender rig T-15 to Seadrill Partners LLC (SDLP) for a total consideration of US$210 million

* Seadrill ordered two jack-ups for a total estimated project price of US$230 million per rig, with deliveries in 4Q 2015 and 1Q 2016

* Seadrill and SapuraKencana joint project secured an eight year contract for three Pipe Laying Support Vessels with a total estimated revenue potential of US$2.7 billion

* North Atlantic Drilling completes sale and leaseback transaction for the newbuild harsh environment jack-up West Linus for US$600 million

Subsequent events

* Seadrill appoints Per Wullf as CEO to take over from Fredrik Halvorsen

* Seadrill orders four ultra-deepwater drillships for an estimated project price below US$600 million per rig, with deliveries scheduled for the second half of 2015

* Seadrill orders two jack-ups for an estimated project price of US$230 million per rig, with deliveries in the second and third quarters of 2016, respectively

* Seadrill reaches 50.1% ownership in Sevan Drilling and launches mandatory offer for all outstanding shares which closed on August 22, 2013

* Seadrill secures a 180 day contract for the newbuild ultra-deepwater drillship West Tellus with a total estimated revenue potential of US$150 million

* Seadrill secures a 2.5 year contract for the jack-up rig West Freedom with a total estimated revenue potential of US$222 million

* Seadrill secures a one year contract extension with Talisman in Malaysia for the jack-up rig West Vigilant at US$167,000 per day

* North Atlantic Drilling is awarded an extension of the current drilling contract, in addition to a new drilling contract for West Navigator, securing employment to December 2014 with a total estimated revenue potential of US$98 million

Click here for complete earnings report and consolidated financial information

Here's a FREE Trend Analysis for SeaDrill....ticker SDRL