The Market Currents staff at Seeking Alpha is shedding some light on the huge write down by Shell this week. Is the U.S. oil boom over hyped?

Shell's (RDS.A) $2.1B write down on its North American shale oil exploration acknowledges some of its spending there will not prove economically viable, and that hitting its cash flow targets could get tougher. Adding to the mystery is Shell's refusal to identify which shale formation has taken the write down or to explain the charge.

Shale skeptics might take the write down as first evidence the U.S. oil boom is overhyped, but WSJ's James Herron thinks it more likely that Shell has "just failed to get lucky" - Eagle Ford, where Shell has significant operations, is well known for its “sweet spots,” which yield greater volumes of the prized liquids compared with gas.

Start trading crude oil today, here's where you start.

Showing posts with label Seeking Alpha. Show all posts

Showing posts with label Seeking Alpha. Show all posts

Thursday, August 1, 2013

Friday, July 20, 2012

Welcome BreitBurn Energy Partners to the COT Fund

Todd Johnson wrote on Seeking Alpha this week....Breitburn Energy Partners offers an enticing 10.2% dividend yield to retirees. The upstream master limited partnership (MLP) generates revenues via natural gas and oil production. I would like to highlight 3 reasons why this MLP has its financials in order to pay out reliable dividends. The 10.2% yield can't be ignored by retirees in the world of a 2.61% 30 Year Treasury Bond yield. Click here to read Todds entire article.

In May equities research analysts at Citigroup lifted their price target on shares of Breitburn Energy from $26.00 to $27.00. The analysts wrote, “BBEP announced on 05/10/2012 that it signed two separate purchase agreements to acquire oil and natural gas properties in the Permian Basin for a combined price of $220 million, subject to customary closing conditions. The acquisition is expected to close within 60 days from the date of the announcement and will be funded with the company’s revolving credit facility.”

BBEP has been the subject of a number of other recent research reports. Analysts at Global Hunter Securities initiated coverage on shares of Breitburn Energy in a research note to investors on Tuesday, April 17th. They set a “buy” rating and a $22.00 price target on the stock. Separately, analysts at Barclays Capital reiterated an “equal weight” rating on shares of Breitburn Energy in a research note to investors on Friday, March 30th. Finally, analysts at Deutsche Bank initiated coverage on shares of Breitburn Energy in a research note to investors on Tuesday, February 14th. They set a “hold” rating on the stock.

But just this week has been upgraded by TheStreet Ratings from hold to buy. With The StreetWire saying....The company's strengths can be seen in multiple areas, such as its robust revenue growth, compelling growth in net income, good cash flow from operations, impressive record of earnings per share growth and notable return on equity. We feel these strengths outweigh the fact that the company shows low profit margins.

BreitBurn Energy Partners is an independent oil and gas limited partnership, focused on the acquisition, exploitation and development of oil and gas properties for the purpose of generating cash flow to make distributions to our unitholders. Our assets consist primarily of producing and non producing crude oil and natural gas reserves located in the Los Angeles Basin in California, the Wind River and Big Horn Basins in central Wyoming, the Powder River Basin in eastern Wyoming, the Evanston and Green River Basins in southwestern Wyoming, the Sunniland Trend in Florida, the Antrim Shale in Michigan, and the New Albany Shale in Indiana and Kentucky.

Historical Dividends

| Declared | Ex-Date | Record | Payable | Amount | Type |

|---|---|---|---|---|---|

| Apr 19, 2012 | May 3, 2012 | May 7, 2012 | May 14, 2012 | 0.4550 | U.S. Currency |

| Jan 27, 2012 | Feb 2, 2012 | Feb 6, 2012 | Feb 14, 2012 | 0.4500 | U.S. Currency |

| Oct 28, 2011 | Nov 7, 2011 | Nov 9, 2011 | Nov 14, 2011 | 0.4350 | U.S. Currency |

| Jul 27, 2011 | Aug 5, 2011 | Aug 9, 2011 | Aug 12, 2011 | 0.4225 | U.S. Currency |

| Apr 28, 2011 | May 6, 2011 | May 10, 2011 | May 13, 2011 | 0.4175 | U.S. Currency |

| Jan 31, 2011 | Feb 4, 2011 | Feb 8, 2011 | Feb 11, 2011 | 0.4125 | U.S. Currency |

| Oct 29, 2010 | Nov 5, 2010 | Nov 9, 2010 | Nov 12, 2010 | 0.3900 | U.S. Currency |

| Jul 30, 2010 | Aug 5, 2010 | Aug 9, 2010 | Aug 13, 2010 | 0.3825 | U.S. Currency |

| Apr 28, 2010 | May 6, 2010 | May 10, 2010 | May 14, 2010 | 0.3750 | U.S. Currency |

| Jan 30, 2009 | Feb 5, 2009 | Feb 9, 2009 | Feb 13, 2009 | 0.5200 | U.S. Currency |

| Oct 29, 2008 | Nov 6, 2008 | Nov 10, 2008 | Nov 14, 2008 | 0.5200 | U.S. Currency |

| Aug 1, 2008 | Aug 7, 2008 | Aug 11, 2008 | Aug 14, 2008 | 0.5200 | U.S. Currency |

| Apr 28, 2008 | May 7, 2008 | May 9, 2008 | May 15, 2008 | 0.5000 | U.S. Currency |

| Jan 29, 2008 | Feb 7, 2008 | Feb 11, 2008 | Feb 14, 2008 | 0.4525 | U.S. Currency |

| Nov 1, 2007 | Nov 7, 2007 | Nov 12, 2007 | Nov 14, 2007 | 0.4425 | U.S. Currency |

| Jul 27, 2007 | Aug 3, 2007 | Aug 7, 2007 | Aug 14, 2007 | 0.4225 | U.S. Currency |

| Apr 26, 2007 | May 3, 2007 | May 7, 2007 | May 15, 2007 | 0.4125 | U.S. Currency |

| Jan 22, 2007 | Feb 1, 2007 | Feb 5, 2007 | Feb 14, 2007 | 0.3990 | U.S. Currency |

Get our Free Trading Videos, Lessons and eBook today!

Monday, April 9, 2012

A Big Mea Culpa About Seadrill's [SDRL] Dividend

From guest blogger Kevin McElroy........

On March 22, 2012 I wrote an article about what I perceive to be a potential danger to investors: a dividend trap. The premise of the article is simple: investors are starved of yield - by design of the Treasury and the Federal Reserve - and Wall Street knows it. So Wall Street will likely conspire to inflate yields to draw investors into stocks.

I pointed out that famed market guru Bruce Krasting noted a tendency of companies to pay dividends from debt. He wrote: "These are referred to as Dividend Deals. The borrower takes on new debt in order to pay a stock dividend to common shareholders. (I prefer to see dividends paid from cash flow from operations, not new debt.)"

I then made a big and frankly pretty stupid mistake with reference to an example of such a company. I talked about Seadrill (NYSE: SDRL), a deep sea driller that pays a substantial dividend with a high level of debt. But I then incorrectly pointed out that Seadrill pays out MORE in dividends than it makes in earnings. I made a mistake of not really digging through the relevant SEC reports to double check my premise.

In hindsight using SDRL as an example of a debt funded dividend payer wasn't the right choice. The metric I was looking at was the company's dividend payout ratio, which based on EPS looks tenuous at best. But as some readers have suggested, a look at cash flow suggests the dividend is more reliable.

One of the keys to Seadrill's dividend success in the future is that the debt to fund expansion of new rigs appears to promise continued growth and sustainable cash flows. This debt vs. growth conversation gets into a broader discussion than I had intended with the article so I won't get into the details.

But I do stand by my point that investors need to be wary about chasing yield and do their homework to understand where those dividends are coming from - my Seadrill faux-pas being just the latest relevant (and professionally embarrassing) example of how easy it is to make foolhardy assumptions about the relevant details.

So let my mistake serve as a lesson to really make sure a company can afford to sustain its dividend.

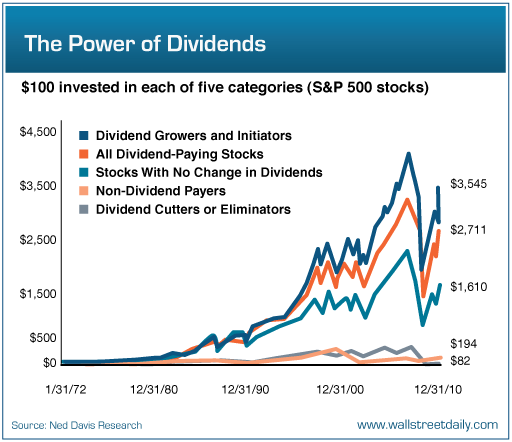

For a final warning of how dangerous it can be to chase yield, take a look at this chart plotting dividend cutters against other classifications of dividend companies:

(click to enlarge)

Being the owner of a dividend cutter essentially means losing money over the long term. So you should avoid companies that have any potential whatsoever of cutting their dividend.

Be careful out there. It's easy to make mistakes. And they're usually expensive.

Follow Kevin's post at Seeking Alpha

Get today's 50 Top Trending Stocks

Subscribe to:

Posts (Atom)